Introducing Synthetix Insights: Issue 1

Dear Synthetix Spartans,

We’re excited to launch “Synthetix Insights” - a newsletter focused on Synthetix, a decentralized synthetic assets issuance and trading protocol that is built on Ethereum. Given the rapid increase usage and following for Synthetix, we see a need for a data-driven approach to provide regular insights to one of the leading DeFi projects in the space.

If you have any feedback, please do let us know at the Synthetix Discord channel.

Synthetic Assets & Derivatives, a Trillion Dollar Market

In this inaugural piece of Synthetix Insights, we are going to start it by exploring why decentralized synthetic assets & derivatives is a major game changer and how Synthetix’s novel design is well-positioned to capture this market.

Synthetic assets refers to financial instruments that replicate the exposure to the underlying asset it is tracking. The exposure can range from price, cash flow and so on. It is usually done through a combination of different financial products such as futures, options and swaps. One might wonder why there’s a need for synthetic assets given that you can just trade the underlying asset? There are few reasons for this which include:

Risk Management: An asset owner can own synthetic assets that give you short exposure to the underlying asset. This allows one to reduce risk by hedging and that might not be possible to do so in spot market.

Leveraged exposure: One can gain leveraged exposure to the underlying asset through synthetic assets such owning a 2x leveraged long ETF of S&P 500 Index.

Ease of access: It’s sometimes easier to short a futures or buy a put option of a financial asset than outright shorting it as it requires borrowing the asset first which might be hard to come by.

In fact, synthetic assets or derivatives volume usually dominate its underlying spot market in traditional financial markets. For example, trading volume of crude oil and gold derivatives are few orders of magnitude higher than its spot physical market as most investors or traders simply want a price exposure to oil and gold without the intention of taking physical delivery or having ownership.

According to the most recent data from the Bank for International Settlements (BIS), the gross market value of all derivatives contracts is approximately $12.7 trillionUSD and daily turnover/volume are more than $10 trillion USD. This is orders of magnitude higher than trading volume of spot financial assets such as stocks, bonds, FX and commodities combined.

We have started to see this playing out in crypto as well. 2018 is the first year where crypto derivatives have traded more volume than the underlying spot market. BitMEX is leading the charge having traded more than $1 trillion USD for 2018. This is despite the bear market in cryptoassets where spot volume has declined compared to 2017.

However it is generally very difficult to bootstrap liquidity for derivatives since you always need one party on the other side of the trade due to its zero sum game nature. BitMEX was launched in late 2014 and only took off in 2018 after attracting many professional market makers to provide liquidity on their platform throughout the years. They also have an internal market making team to provide liquidity for various derivatives contract on their platform.

When it comes to bootstrapping liquidity on a decentralized synthetic assets trading platform, a similar approach is much more difficult as most professional market makers need to interact with smart contracts directly and deal with latency of the blockchain. Additionally the volume of new decentralized exchanges are usually too little at the beginning for professional market makers to justify investing resources in it.

Synthetix use a novel approach to tackle this lack of liquidity issue that is prevalent among many decentralized exchanges. Instead of spending significant resources to support an in-house market making team, SNX minters that issue synthetic assets by staking their SNX act as a pooled liquidity provider to every trade that happen on Synthetix Exchange. This pooled liquidity model enable Synthetix to leverage on the strength of its community to provide unparalleled liquidity right from the start. SNX minters collectively are rewarded all the transaction fees generated from trading activity on Synthetix Exchange for taking on the risk of being a liquidity provider.

Additionally, using SNX as collateral to generate synthetic assets allows the supply of synthetic assets to scale with the demand, since the value of SNX are intrinsically dictated by the fees generated from Synthetix Exchange. More demand for synthetic asset trading will lead to higher value of SNX token thus leading to more synthetic assets able to be issued. This novel design aligns the incentives between synthetic assets issuer and users.

Using external assets such as Ether to generate synthetic assets will not have the benefits above. For example DAI is a by-creation of self-leverage demand, DAI issuers do not have any direct incentives for issuing DAI except for their own demand to leverage on their Ether holdings or to generate some cash without giving up their upside in Ether, instead they are paying a higher than market interest rate for this over-collateralized borrowing. The incentives for DAI issuers to issue more DAI are not very strong even if DAI is trading at a premium if DAI issuers don’t want to take on more leverage.

Overall, Synthetix represents a game changer in decentralized synthetic assets issuance and trading space. We see a huge potential for it grow further as it get more system wide integration and people slowly realize the potential of censorship resistant and permissionless ownership of various synthetic assets.

The SNX Liquidity Myth

It probably goes without saying, that liquidity is extremely important when considering investments.

The simplest and most straight-forward rationale is that illiquidity hides true value and the current market price might not be reflective of what you can actually buy or sell at.

A few trades matched with tiny volume is an outlier, while lots of trades matching with high volume makes for a more reliable price.

One of the common criticisms of SNX as an investment is that it is extremely illiquid. However, we are going to show why this is not true.

Firstly, SNX volume is constantly underreported due to the simple fact that almost all websites and services that track volume are only looking at centralized exchanges. However the majority of the volume of SNX is actually taking place on Uniswap and Kyber, and this data is usually not reflected. CoinGecko is one of the few tracking sites that is able to capture this data, and just comparing the previous 24hr vol, CMC is under-reporting volume by ~50%.

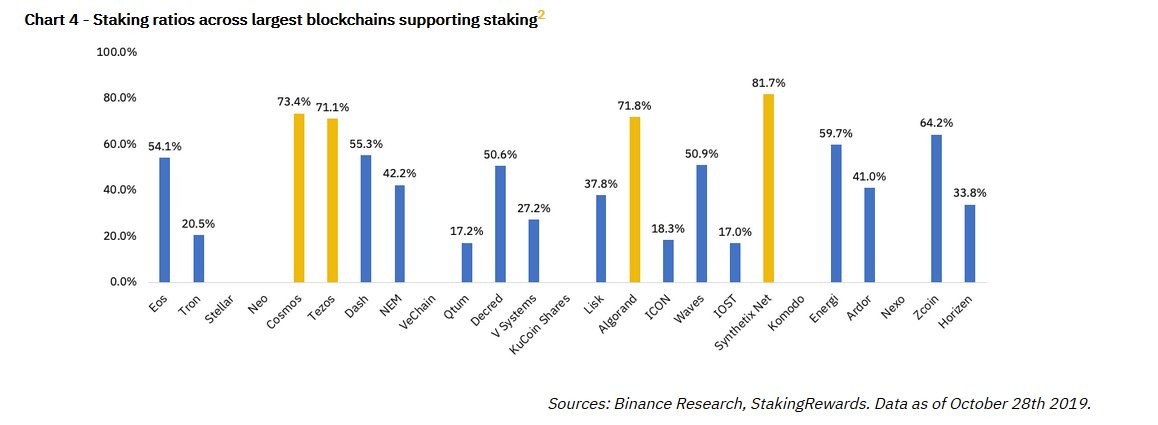

Next, take into account that SNX is a staking token that has extremely high staking participation rate due to very attractive rewards from its monetary inflation schedule. From the latest research published by Binance Research on Staking, Synthetix has the highest staking ratio across the largest fifteen crypto-networks by market capitalization.

With the staking rewards standing at 75% APR for the first year. Few SNX holders are willing to engage in market making activities or trading their SNX holdings around when the opportunity cost of not participating in staking is high.

The effect is that less than 2% of supply can be traced to exchange wallets as user deposits which are available for trading. Slightly over 0.5% of the supply is in Uniswap, but due to the constant product pricing model, it is impossible to drain out the SNX there without ending up paying obscene prices.

It’s also misleading to look at volume alone to assess liquidity of a cryptoasset, depth of the buy/sell order book is a much more important metric to look at as that represent the actual cost of entering and exiting the asset. It is also harder to fake compared to trading volume which is frequently gamed by many exchanges listed on CoinmarketCap.

SNX currently has the 5th largest Uniswap pool standing at $1.5m of liquidity, a 10,000 SNX sell order on Uniswap will only incur a 3.4% of slippages, which is slightly higher than cryptoassets at similar market cap, but by no means completely illiquid.

Uniswap have also become the primary source of liquidity for SNX. SNX is one of the very few top 100 cryptoassets that have more liquidity on decentralized exchanges than centralized exchanges besides MKR and DAI. This makes the SNX liquidity much more robust and less susceptible to the whim of any centralized exchanges.

SNX also experienced a major stress test on its liquidity on 26th October where one of the top 50 token holders sold his entire 324k SNX holdings in less than 15 hours on Uniswap. While this major selling did cause the price to correct around 30% afterwards immediately, the combination of cross-exchange arbitrage and organic buying demand at that level lead SNX to close the day only down 15%, and back to similar price level before this major selling occurred in 1 week.

To put this into context, during the 17th May flash crash of Bitcoin price, it only took a sell order of 4,300 BTC to crash the Bitcoin price on Bitstamp by more than 20%, and the 50th top holder of Bitcoin holds 14,500 BTC.

Given the high opportunity of not staking SNX, most big tickets trade size occurs through over-the-counter (OTC), as large holders are actively staking and will only unstake when there is a confirmed buyer/deal in place. According to one of the leading OTC brokers, SNX has much better OTC liquidity compare to cryptoassets with similar market cap.

By buying or selling SNX through OTC, buyers/sellers are able to deal quickly to minimize opportunity cost lost by breaking up orders. The recent availability of OTC tools (Deversifi Trustless OTC/ Airswap Trader) also make the entire OTC process much more efficient and trustless.

There is an OTC channel in SNX Discord that helps mid size SNX holders to find a match and deal trustlessly, together with several OTC brokers actively helping to facilitate various deal size with both trustless and trusted escrow methods

Below is some of the on-chain OTC trades we managed to identify:

Deversifi Trustless OTC

55,243 USDT for 123,750 SNX

https://etherscan.io/tx/0x2c13f69959f465063ee80f209c15eba2c8bf9d0b54ca58f3276aeee4e947519a

406.9186 Ether for 110,000 SNX

https://etherscan.io/tx/0x56d372f43e08859531bb394658d7c763e7bc725a80c12ed177bee74b51ae0187

500 ETH for 71,118.7734 SNX https://etherscan.io/tx/0x38ec203c3b79f270f62361cae298baeb1d688e27cf5c52f9fd0ccc1b91642e11

500 ETH for 64,923.0128 SNX https://etherscan.io/tx/0xc4718724c66905c137e6be615c48426726b14f6a36e0c369ca9a454840ad9cf5

Airswap Trader

300k USDC for 400k SNX

https://etherscan.io/tx/0x81e60c0da3b09b219df284cd39e76b14633f85d1621120050a67520287912147

395 ETH for 100k SNX

https://etherscan.io/tx/0x94d0e85fc75534dd7918e2e7bf05b5fd51157a8f7bfa7d78a63066d03ba4a5ba

395 ETH for 100k SNX

https://etherscan.io/tx/0x5136ade186c8186ba475c05c9f237de8b6a814c00a86de00a71867a6113cc6bc

395 ETH for 100k SNX

https://etherscan.io/tx/0x5570920896d795f6853b69f43cfa2eb3b95d5e593eb300592985ff3a9ba3ed3b

73,500 USDC for 100k SNX

https://etherscan.io/tx/0x209424cbc2414d016df9fb9e34910732cdfbcb0e536080112f288fad9dc744d9

$111,720 USDC for 100k SNX https://etherscan.io/tx//0x0e415803d75d57f4d4919c375a784b2aa8c9bde6505023f285bd18b0dade6639

Therefore, SNX is actually much more liquid than it appears on the surface with ~$500K USD daily volumes.

Network Data Insights

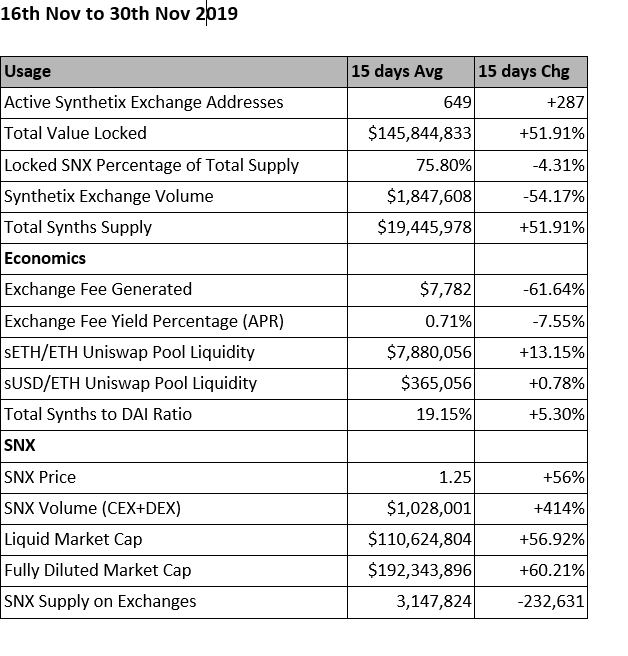

SNX rallied significantly over the last 2 weeks, recorded a gain of 56% compared to the average price of SNX for 1st half of November 2019. The volume for SNX increased even more standing at average volume of roughly $1m/day compared to $200k/day previously. Synths supply expanded significantly as well to as people are able to mint more given high value of their SNX holdings. However interestingly the SNX supply on exchanges have actually come down despite the price increase, shows that new SNX buyers are withdrawing it from their exchange to stake instead of just for pure speculation reason.

The Synthetix Exchange metrics present a mixed numbers, the active traders have increased significantly to 649 unique address trading on Synthetix Exchange over the last 15 days. However volume has come down due to the increased trading fees to 0.5%, we expect it to climb up again given the fee has been lowered down to 0.3% lately.

The sETH/ETH Uniswap pool liquidity continues to increase despite the drop in ETH price lately, it reached as high as $9m right now and shows no sign of stopping as the yield continue to increase with the climb of SNX price. One metric we will be watching closely is the total synths to DAI ratio as it represent an entirely different system design to bootstrap a synthetic asset issuance system.

Recent Discord Discussions

- Ether collateral and specific implementation details

- Smoothening of current inflation schedule + tail end emissions (see SIP draft)

Upcoming milestones

- Synths Lending on bZx and Aave

- Synthetix Exchange v2

- More Community SIPs approval and integration

Recent announcements

Arcturus Release

Knowledge Base

The Ultimate Guide to Synthetix

Balance Sheet as a Business Model for DeFi Platforms

Synthetix's Kain Warwick: How Ethereum Will Absorb a Trillion Dollar Market

TwiceCrypto Beginner's Guide to Synthetix (Jun 19) *Updated*

The Block's coverage of Synthetix (Jun 19)

Future of DeFi Panel - NY Blockchain Week (Jun 19)

Overview of the current state of Synthetix by Micky (Jun 19)

NASDAQ interview with Kain at BlockchainNYC (May 19)

Subscribe and Past Issues

Synthetix Insights is an data driven bi-monthly newsletter on the state of Synthetix, a decentralized synthetic asset issuance and trading protocol. If you'd like to get Synthetix Insights in your inbox, please subscribe here.