Synthetix Insights: Issue 2

Dear Synthetix Spartans,

It’s been a wild couple weeks since our first issue in December. At one point, SNX was down nearly 50% from its highs and the network’s collateralization ratio was well under target. But, despite a couple of panicked sellers and Twitter skeptics, the team has kept building, while stakers and traders have nursed the network back to health.

With the feature-filled Achernar release on the horizon, we wanted to hit a number of topics in this issue. We have four contributor pieces, each on an important subject to the future of Synthetix:

@mjayceee on one potential risk of ETH collateral and how to manage it

@gmgh on the new automated Uniswap sETH pool rewards contract

Jaaq (@snxwhalewatch) on how Synthetix stakers reacted to the major price drop (preview: the system worked as designed)

And finally, Garth, the @synthetix_io Community manager, with an update from the team on the upcoming release

One Risk of Ether Collateral

I wrote a piece a couple of weeks ago about the implications of adding Ether as collateral on Synthetix and why it may be critical to the success of the project. You can read it here.

While the Synthetix team has given us no reason to believe that they can’t execute on ETH collateral, the feature will absolutely make the system more complicated. There will be new attack vectors, sure, but also there will be new systemic complexities that we may not fully understand yet.

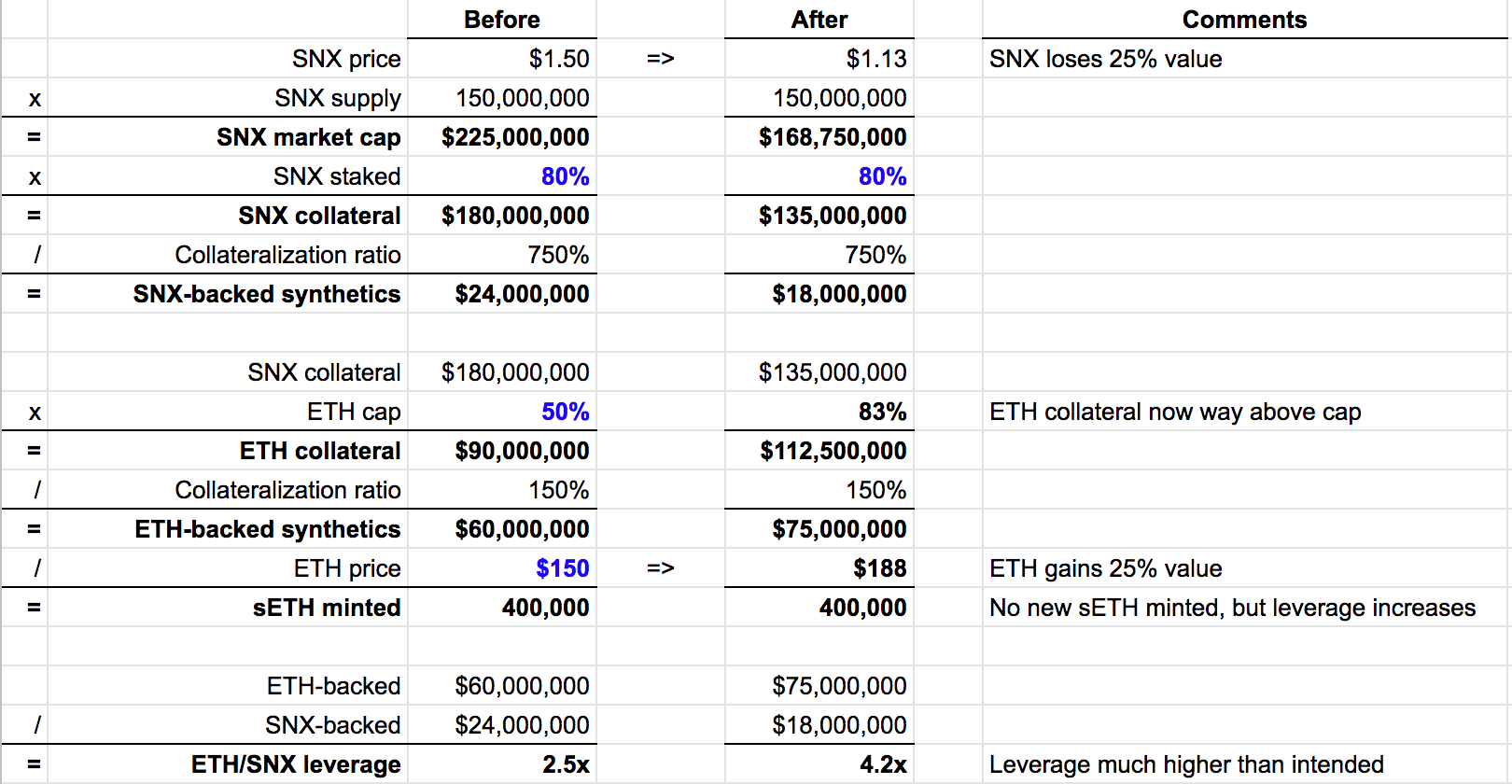

One complexity that I think is interesting to explore is the possibility that the prices of ETH and SNX diverge aggressively. Consider this scenario: ETH-collateral traders have minted sETH on up to 50% of the value of SNX collateral, approaching a hypothetical 50% cap set by the community. There are now $2.50 of ETH-backed synthetics for every $1 of SNX-backed synthetics (see exhibit below for the math).

This imbalance is okay. We need some leverage for the system to generate enough fees for the concept to work. The article linked in the first paragraph discusses this at length.

But say, for whatever reason, the prices of SNX and ETH diverge, with SNX losing 25% of its value and ETH gaining 25%. The protocol has capped new sETH minting at 50% of SNX collateral, but if the liquidity is already issued, there’s no obvious lever to quickly restore a 50% ratio. In the case below, there are now $4.20 of ETH-backed synthetics for every $1 of SNX-backed synthetics. The 50% ETH collateral cap has been forcefully breached and has run up to 83%.

Pre-debt staking/trading yield will certainly be higher with more liquidity paying less SNX collateral. But risk will be much higher as well. At unintended levels of leverage, stakers will feel the impact of a particularly successful year for Synthetix Exchange traders more acutely.

The probability of stakers falling into debt isn’t necessarily higher or lower at elevated leverage. The variability, however, is much higher. As leverage increases, the probability of exposing systemic weaknesses in the system grows.

Fortunately, the team and community are committed to a gradual rollout of ETH collateral, where weaknesses and potential exploits can be sussed out while the stakes are lower. And even if a scenario like the one above comes to pass, a 4.2x leverage ratio is probably still in the safe zone. The key is capping ETH collateral at a level where even a wide divergence leaves the system in a manageable state.

SIP-31: The New sETH LP Rewards Contract

In July 2019, the Uniswap sETH Pool Liquidity incentives were announced on the Synthetix Blog after much discussion within the community.

Uniswap — being a permissionless liquidity protocol — made it such that Synthetix could make use of the broader Ethereum ecosystem to increase the economic bandwidth moving in and out of the Synthetix. The goal of the incentives was to drive a deeper liquidity pool that would minimize the friction of traders moving in and out of the system. Liquidity providers would be given incentives in SNX based on their contribution.

The pool has blown away even the most optimistic expectations of community members and now is by far the largest pool on Uniswap, standing well north of 40,000 ETH and 40,000 sETH (source: SynthetixStats).

The pool incentives were formalized with SIP-8 in August 2019, where an off-chain script had to be run to verify Liquidity Pool participants, their contribution and their dues. Due to the limitation of the script, it is not easy to detect edge cases of possible "cheating", whereby participants shift, redeem or burn LP tokens in an effort to still qualify for rewards, while not truly participating in liquidity provision. Perhaps the most arduous part of finalizing the incentives every week is coordinating the multi-sig signers to broadcast the signed transaction after manually verifying the validity of participants and their rewards. This is further exacerbated by the huge increase in liquidity pool participants, as well as the gnosis multi-sig freezing from such a large data payload.

Essentially, it was a very manual process that does not scale well as this programme grew in participation and is less than ideal due to the reliance on several human factors. This is where SIP-31 comes in.

Under this new specification, LP tokens that are generated when liquidity providers send in liquidity, would be staked into a special smart contract "Uniswap Time Staking Contract". LP token stakers would then have to manually call the contract to receive their rewards, which do not expire.

This new method of distributing the rewards is a massive step towards the right direction, since it removes the need for an offline script to track the accounting of rewards, the possibilities of cheating the system is neutralized, and it shifts the burden from a push by the multi-sig signers into a pull by the user, eliminating the human element in the equation.

The result of this SIP-31 is a more elegant, scalable and long term design for rewarding liquidity provision of any Synth or even SNX pooling through a Uniswap-like protocol which generates a Liquidity Token receipt.

Overall, this is an excellent SIP which demonstrates quite clearly the power of having the ability to iterate on designs. It sets the stage for future similar style of liquidity rewards by overcoming the technical hurdles, which this refined proposal is the direct result of.

Analyzing the Synthetix Stress Test

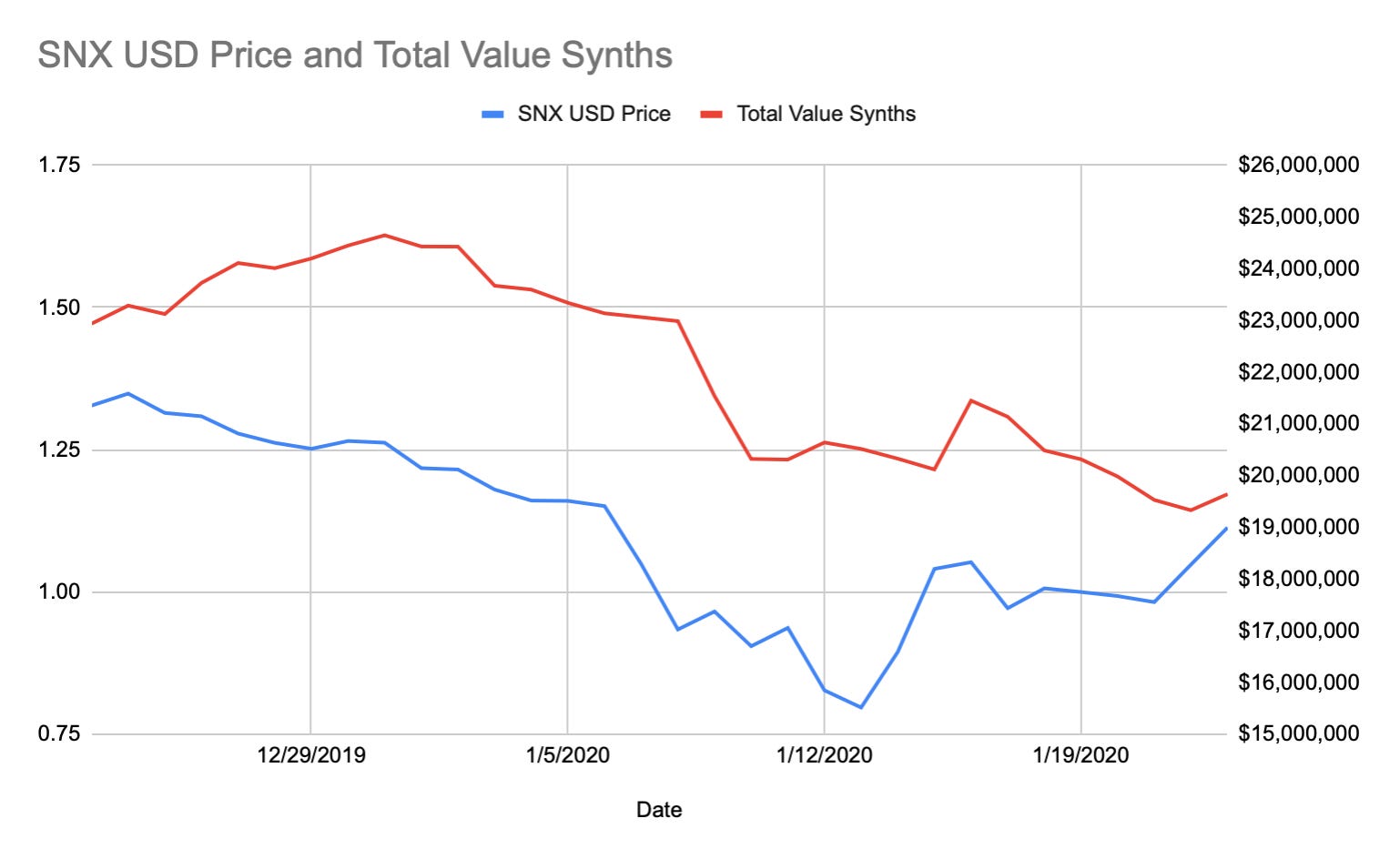

The new decade started of with turbulent price action for Synthetix, with the SNX token price declining steadily at the end of December. Shortly after the new year, things accelerated and SNX plunged to a low of around 80 cents, after reaching an all-time-high of $1.58 in November — a correction of 50%.

Since the SNX Token is currently used to collateralise all of the outstanding synthetic assets, it’s important to take a closer look at how the system performed under this stress test. With no liquidation mechanism in place, it’s fully up to the minters to maintain a healthy c-ratio, as the only penalty for being under collateralized is the inability to claim weekly rewards.

Looking at the graph below, we can conclude that the performance of the system was nothing short of stellar. As the SNX token dropped in price, minters were not willing to forfeit their rewards for having a sub 750% c-ratio, and they burned their synths accordingly. As the SNX price slowly climbs up again, the total synths value is beginning to follow suit as more synths are being minted again.

Team Update

The team’s heads are down again and we’re straight back into #ExpressShipping mode, especially after the ambitious roadmap published here. We’ve just announced that due to the amount of time it will take for each critical item to be audited, Achernar will be deployed at some stage in early February.

If you haven’t already read it, you should check out Kain’s article on the current state of Synthetix. He explains the difficulty of running a crypto startup (compared to the already difficult task of running a regular startup) due to the totally untouched surface area of intersecting governance, tokenomics, and smart contracts. Moving forward, the project needs to assess all aspects of the system in relation to two parties: stakers and traders. Determining which updates are made to the system must be done only after careful consideration of how both parties will be affected, as improving the experience in the most obvious way for one can often have trade-offs for the other party.

The next few releases (Achernar, Betelgeuse, and Hadar) will help ensure the system is in a much stronger place, for stakers, traders, and people looking at the system from the outside for the first time, whose first questions are often concerned with using Ether as collateral, liquidation mechanisms, and who controls oracles. We look forward to collaborating with the community to bring the project further into focus for the growing attention on the DeFi ecosystem.